The latest release for China’s Manufacturing PMI was released, here the highlights:

• New export business declines at sharpest rate in nearly two years

• Employment falls for the nineteenth month in a row

• Deflationary pressures ease

Operating conditions in China’s manufacturing sector continued to deteriorate in May, as companies signalled a renewed contraction of output as total new business fell for the third month running.

Data suggested that weaker demand overseas was a key factor behind the latest fall in new business, as new export work declined at the steepest rate since June 2013.

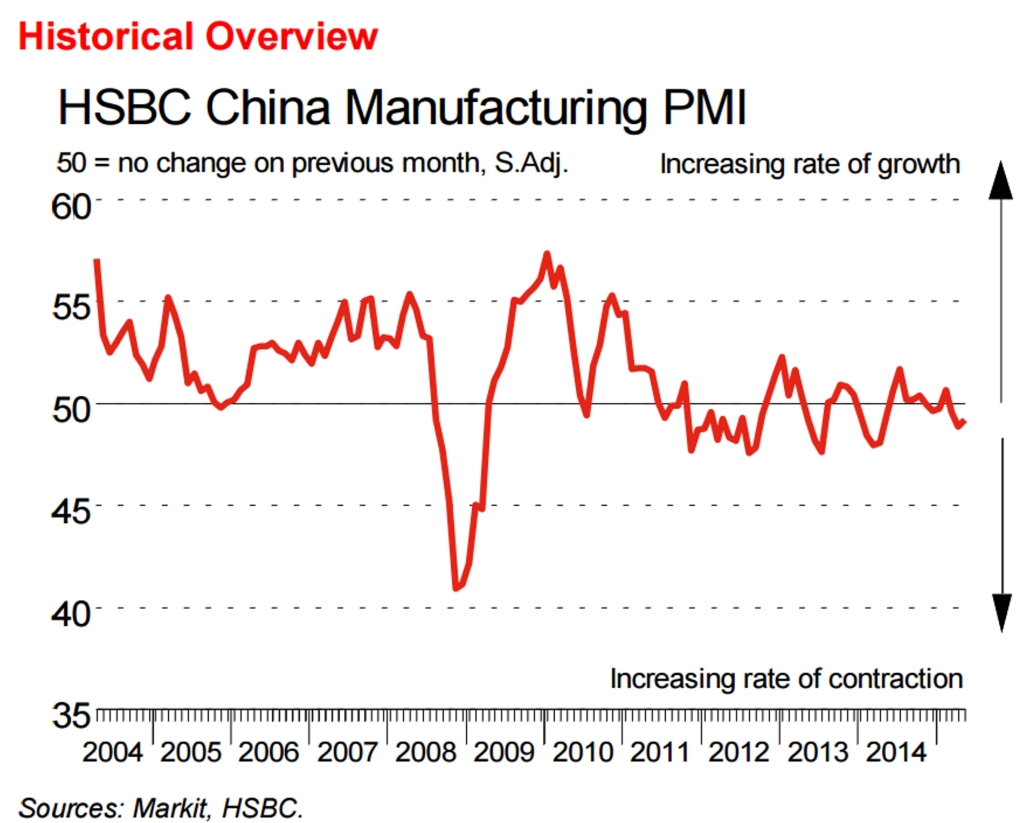

Deflationary pressures in the sector eased, with both input and output prices recording the slowest rates of deflation since August 2014. The HSBC Purchasing Managers’ Index™ (PMI™) posted at 49.2 in May. Although this was up slightly from 48.9 in April.However, the rate of deterioration remained only slight.

May data signalled a renewed fall in Chinese manufacturing output, after production volumes stagnated in April. Although the rate of decline was only marginal, it was the first time that output had contracted since last December.

Total new business placed at Chinese manufacturers has now fallen for three successive months. Data suggested that weaker demand from abroad was the main factor behind the latest reduction in new work. Moreover, the latest fall in new export business was the sharpest in nearly two years.

Manufacturers tempered their production plans in line with fewer new orders in May, with purchasing activity falling for the second month in a row. Consequently, stocks of purchases fell in May, though the rate of depletion was only slight.

Employment at Chinese goods producers declined again in May, extending the current sequence of job shedding to 19 months. According to anecdotal evidence, lower production requirements and the nonreplacement of voluntary leavers led to reduced staff numbers.

Backlogs of work rose fractionally over the month, after a slight reduction during April. Average input costs fell again in May, albeit at the weakest rate in nine months. Prices charged also fell in May but, in line with the trend for cost burdens, the rate of discounting eased to its slowest since August 2014.